August 30, 2025

NVIDIA overview

NVIDIA is a U.S.-based technology company best known for designing graphics processing units (GPUs). Its chips power everything from video games to artificial intelligence, data centers, self-driving cars, and robotics.

The company began by building GPUs for PCs and gaming consoles, but later expanded into AI and data centers, where its chips have become critical for training and running large AI models, such as ChatGPT. NVIDIA is also active in automotive technology, providing hardware and software for driver-assistance systems, as well as in supercomputing and robotics.

Recent developments

In August 2025, a U.S. District Judge in California ruled that a lawsuit filed by Mercedes-Benz supplier Valeo against NVIDIA has sufficient evidence to proceed to trial. The case, scheduled for November 2025, alleges that NVIDIA benefited from trade secrets misappropriated by a former Valeo engineer. NVIDIA denies the allegations, stating it has “no reason to” steal proprietary information. The outcome of this trial could have significant implications for NVIDIA’s relationships within the automotive and technology sectors.

In a separate development, NVIDIA has suspended production of its H20 AI chip following pressure from Chinese authorities urging local firms to avoid U.S. semiconductors over security concerns. This move highlights the growing geopolitical risks facing NVIDIA’s operations in China and underscores the company’s vulnerability to U.S.–China tensions.

Despite these challenges, analysts at J.P. Morgan have reaffirmed their optimistic stance on NVIDIA, raising their target stock price to $215. This bullish outlook is driven by NVIDIA’s growing artificial intelligence infrastructure pipeline and the rollout of new products, which are seen as key factors for future growth. The analysts believe that these elements offer multiple opportunities for the company to exceed expectations.

The numbers

Revenue ($M): 46,743 (Q2 FY26), 44,062 (Q1 FY26), 30,040 (Q2 FY25)

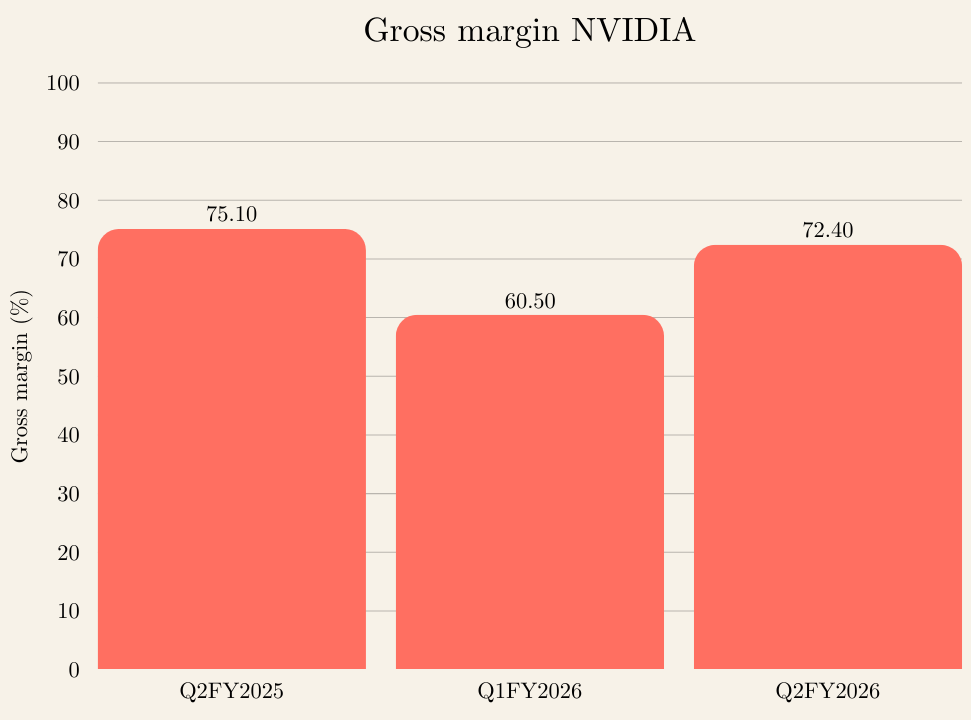

Gross Margin: 72.4% (Q2 FY26), 60.5% (Q1 FY26), 75.1% (Q2 FY25)

Operating Expenses ($M): 5,413 (Q2 FY26), 5,030 (Q1 FY26), 3,932 (Q2 FY25)

Operating Income ($M): 28,440 (Q2 FY26), 21,638 (Q1 FY26), 18,642 (Q2 FY25)

Net Income ($M): 26,422 (Q2 FY26), 18,775 (Q1 FY26), 16,599 (Q2 FY25)

Diluted EPS ($): 1.08 (Q2 FY26), 0.76 (Q1 FY26), 0.67 (Q2 FY25)

Source: NVIDIA august 27, 2025

Behind the numbers

NVIDIA reported strong revenue growth, reaching $46.7 billion in Q2 FY26, up 6% from the previous quarter and 56% from a year ago. Net income rose to $26.4 billion, while diluted EPS jumped to $1.08, reflecting robust earnings per share growth.

The most striking feature of this quarter is the gross margin increase from 60.5% to 72.4%, an unusually large jump for a company of this size. This shows NVIDIA is keeping significantly more profit from each dollar of revenue. The increase was driven by high-margin AI products, particularly the Blackwell Data Center chips, and the release of previously reserved H20 inventory, which added revenue without substantial additional costs.

Operating income grew 31% quarter-over-quarter, outpacing revenue growth and demonstrating that NVIDIA is scaling efficiently — more of its sales are translating into profit.

Overall, this quarter highlights NVIDIA’s strong profitability and efficient growth, with AI-focused products driving both revenue and unusually high margins.

Outlook and key considerations

NVIDIA’s growth outlook remains strongly tied to AI and Data Center demand, with the launch of Blackwell Data Center chips positioning the company at the center of the fast-growing AI infrastructure market. The unusually high gross margin in Q2 FY26 is noteworthy, but investors should understand that part of the increase comes from a one-time effect: NVIDIA was able to sell H20 AI chips that had been produced earlier but held back from sales due to restrictions in China.

Since these chips were already made, their sale added revenue without substantial new costs, temporarily boosting profitability. In addition, the company’s future gross margin could vary depending on the mix of products sold—if lower-margin products like gaming GPUs make up a larger portion of sales, overall profitability could be lower.

Geopolitical risks, particularly restrictions on chip sales to China, could affect revenue and profitability. NVIDIA also faces competition from AMD, Intel, and cloud providers developing their own AI hardware, which may pressure prices or market share. Despite these considerations, NVIDIA remains highly valued, with a PE ratio of around 49.4, reflecting strong earnings growth, though the decreasing trend suggests the market is pricing in slightly more caution.

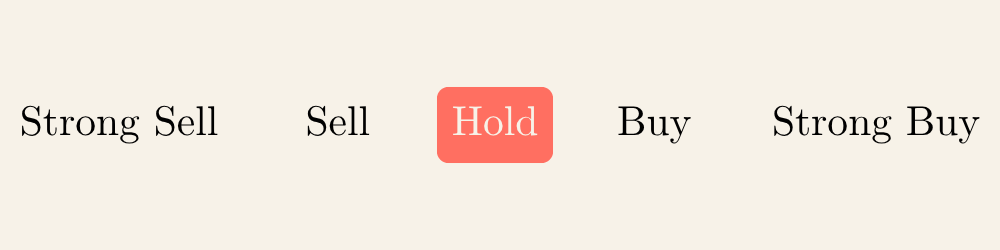

Recommendations: Hold

NVIDIA continues to perform strongly, driven by robust revenue growth, high demand for AI products, and its innovative Data Center chips. The company demonstrates clear leadership in AI infrastructure and high profitability.

However, investors should be aware of risks. Geopolitical restrictions on chip sales to China and competition from AMD, Intel, and cloud providers could affect revenue and market share. NVIDIA is also facing a lawsuit from Mercedes-Benz supplier Valeo, which could have implications for its automotive and technology partnerships.

Despite these considerations, the stock is highly valued, with a PE ratio around 49.4. Given the strong performance but elevated valuation, the prudent approach is to hold existing positions and await a better entry point.

This outlook is based on a 12- to 18-month view. This analysis is for informational purposes only and does not constitute professional investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.

Subscribe to the newsletter!

With the Augustyn Analytics Newsletter, you receive a clear monthly update featuring key business news highlights, our latest investment analyses and recommendations, a new entry from the Investor’s Guidebook explaining essential financial terms, and important updates from the Augustyn Analytics platform. Delivered just once a month, it is designed to keep investors up to date.