August 1, 2025

Microsoft overview

Microsoft (MSFT) is one of the largest tech companies in the world, known for products like, Windows, Office, Azure cloud services, and its growing investments in AI. It operates in enterprise software, cloud computing, gaming (Xbox), and productivity tools.

This analysis follows the company’s Q2 FY2025 earnings release, which investors are watching closely for signs of AI-driven growth and how the company is handling rising competition across the tech sector.

Recent developments

Microsoft has been at the center of the AI boom, largely due to its deep partnership with OpenAI and the rapid roullout of Copilot – AI tools now embedded into products like Word, Excel, and Teams. These features are designed to boost productivity and are already being adopted by businesses across industries.

To support this AI push, Microsoft plans to invest around $80 billion between 2025 and 2028 in building new data centers globally. These facilities are optimized for AI workloads, powered in part custom silicon and renewable energy. It is on of the largest infrastructure efforts in the company’s history.

At the same time, Microsoft continues to compete for market share in cloud computing. Azure, its cloud platform, is currently the second-largest behind Amazon Web Services, with Google Cloud in third. As AI demand grows, investors are closely watching whether Microsoft can sustain its momentum across software, cloud, and infrastructure.

The numbers

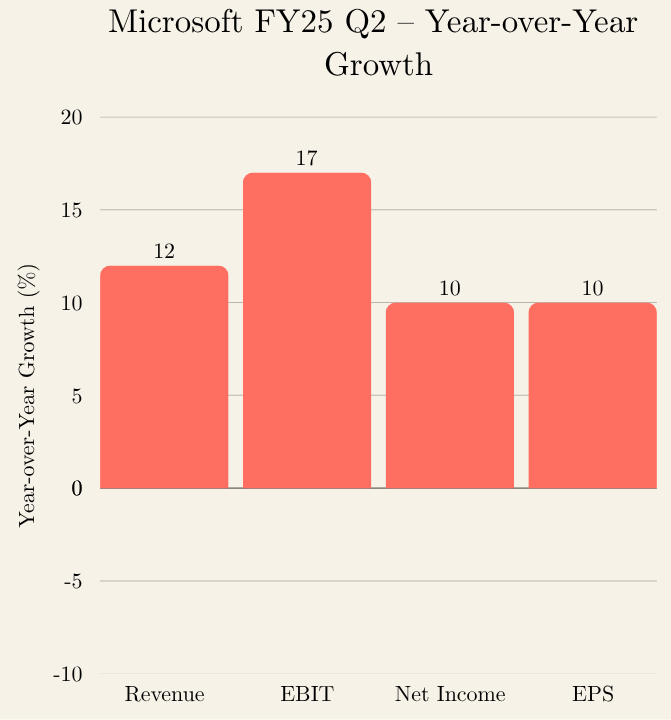

In Q2 of fiscal year 2025 (ended December 31, 2024), Microsoft reported strong results across the board:

Revenue was $69.6 billion and increased 12%

Operating income (EBIT) was $31.7 billion and increased 17%

Net income was $24.1 billion and increased 10%

Diluted earnings per share (EPS) was $3.23 and increased 10%

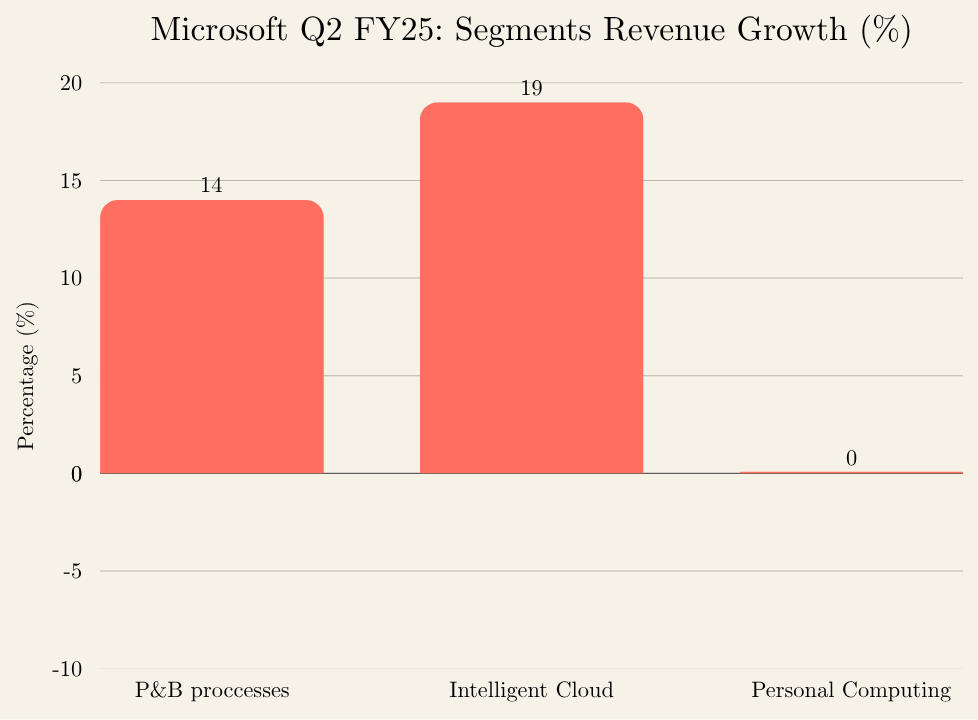

Microsoft divides its business into three main segments, each contributing differently to the company’s overall growth. Productivity and Business Processes generated $29.4 billion in revenue, an increase of 14% compared to last year. Intelligent Cloud delivered $25.5 billion in revenue, up 19% year-over-year, driven by strong demand for Azure and AI services. Meanwhile, More Personal Computing brought in $14.7 billion, remaining relatively flat as growth in Windows and advertising was offset by weaker gaming results.

In addition to these results, Microsoft returned $9.7 billion to shareholders through dividends and share repurchases during the quarter. The company also highlighted rapid growth in its AI business, which has now reached an annual revenue run rate of over $13 billion — up 175% from a year earlier.

Behind the numbers

Microsoft’s 12% revenue growth reflects strong demand across its core businesses, particularly cloud and AI services, which continue to drive expansion. The 17% increase in operating income indicates the company is improving profitability by managing costs effectively while scaling its operations efficiently.

Net income grew 10%, matched by a 10% increase in diluted earnings per share (EPS), meaning Microsoft is not only generating higher overall profits but also delivering greater earnings per share to its shareholders. This demonstrates strong financial health and effective capital management.

Together, these results show Microsoft’s ability to grow both revenue and profits simultaneously, balancing investment in innovation with operational discipline. The steady increase in earnings per share reinforces confidence in the company’s ability to create shareholder value over time.

Additionally, Microsoft returned $9.7 billion to shareholders through dividends and share repurchases during the quarter, highlighting its strong cash flow and commitment to rewarding investors—actions that can boost shareholder confidence and stock value. Meanwhile, the AI business’s rapid growth—up 175% to a $13 billion annual revenue run rate—underscores Microsoft’s successful investment in a high-potential area, positioning the company well for future growth.

Outlook and key considerations

Microsoft is well-positioned for continued growth, driven by strong demand for cloud and AI services. The AI business, now generating over $13 billion annually, is a key driver for future expansion. Ongoing strength in productivity software and cloud infrastructure supports a positive long-term outlook. The company’s broad product portfolio, leadership in Azure, and integration of AI across tools like Microsoft 365 and Dynamics 365 provide a strong foundation. Its recurring revenue, loyal customer base, and solid balance sheet enable continued investment and shareholder returns.

However, Microsoft faces risks that could impact its growth trajectory. Intense competition from tech giants such as Amazon and Google in cloud and AI markets could pressure margins and market share. Regulatory challenges in multiple regions pose potential hurdles, and macroeconomic uncertainties may affect enterprise IT spending. Furthermore, the fast pace of technological change requires Microsoft to continuously invest in innovation to maintain its competitive edge. Balancing these strengths and risks will be crucial for Microsoft’s ability to sustain growth in the coming years.

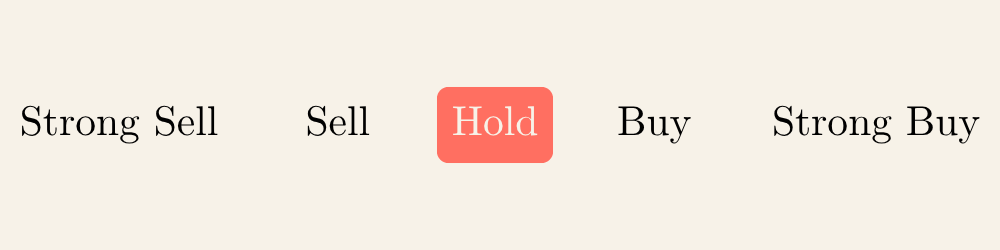

Recommendation: Hold

Microsoft remains a high-quality business with strong momentum in cloud and AI. Its steady revenue growth, solid profitability, and leadership in key tech trends support long-term confidence in the company.

While the stock may still see modest gains in the future, it is already trading at a high valuation — with a P/E ratio around 40 — reflecting a lot of optimism about future growth. Much of that optimism is already priced in. For this reason, we believe it’s wise to Hold the stock for now and wait for a more attractive entry point before considering a new investment.

This outlook is based on a 12- to 18-month view. This analysis is for informational purposes only and does not constitute professional investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.