September 6, 2025

Philips overview

Philips is a Dutch health technology company headquartered in Amsterdam. Founded in 1891 as a lightbulb manufacturer, it has transformed into a global leader in medical technology and personal health products. The company operates in three main segments:

- Diagnosis & Treatment – Imaging systems such as MRI, CT, and ultrasound scanners.

- Connected Care – Patient monitoring systems, ventilators, and digital health solutions.

- Personal Health – Consumer products like electric toothbrushes, shavers, and sleep therapy devices.

Philips shares are listed on both the Amsterdam Stock Exchange (ticker: PHIA) and the New York Stock Exchange (ticker: PHG).

Recent developments of Philips

Philips is strengthening its U.S. presence with more than $150 million in new investments. The company is expanding its manufacturing facility in Reedsville, Pennsylvania, where it produces AI-enabled ultrasound systems, and adding new space for research and warehouse operations, creating around 120 skilled jobs. At its Plymouth, Minnesota site, focused on image-guided therapy, Philips is adding over 150 new roles. These expansions support the company’s strategy to grow key health technology areas and bring innovation closer to the U.S. market.

A major challenge for Philips was the 2021 recall of CPAP, BiPAP, and ventilator devices due to degrading foam that could harm patients. In April 2024, the company reached a $1.1 billion settlement for U.S. personal injury and medical monitoring claims, without admitting liability. The settlement reduced legal uncertainty, and Philips’ shares rose as the financial risk proved lower than expected.

Philips has also been affected by trade tariffs. Following a U.S.–EU trade agreement announced on July 27, 2025, which set a 15% tariff on most EU imports, the company reduced its projected tariff-related costs for 2025 from €250–300 million to €150–200 million, while also adjusting its supply chain to maintain profit margins.

The numbers

Revenue ($B): 17.86 (2025), 18.02 (2024), 18.17 (2023)

Gross profit Margin (%): 43.84 (2025), 43.13 (2024), 40.99 (2023)

Operating Margin (%): 6.03 (2025), 2.85 (2024), -0.92 (2023)

EBITDA ($B): 2.32 (2025), 1.77 (2024), 1.00 (2023)

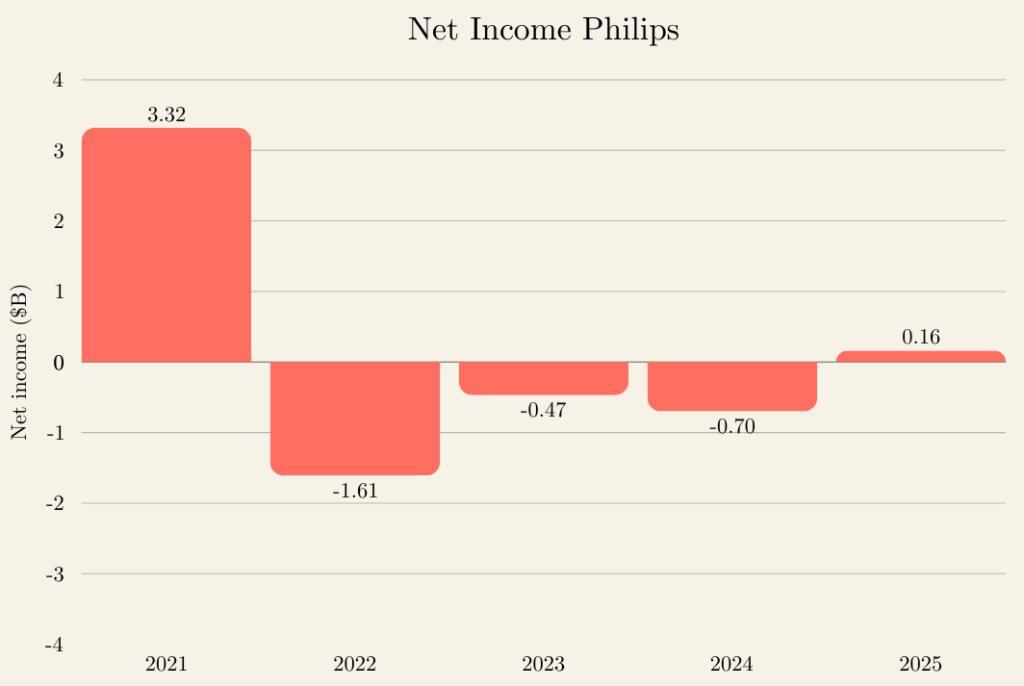

Net Income ($B): 0.16 (2025), -0.70 (2024), -0.47 (2023)

Normalized EPS ($): 1.44 (2025), 1.38 (2024), 1.21 (2023)

Dividends per share ($): 0.85 (2025), – (2024), – (2023)

Source: Morningstar September 5, 2025

Behind the Numbers

Philips’ recent financials show a clear story of recovery. Revenue has remained relatively stable around $18 billion, while gross profit margins are consistent at roughly 41–44%, reflecting good control over production costs. Operating income and EBITDA have been gradually improving, indicating stronger operational efficiency.

Net income, however, tells a different story. The company reported negative net income in 2023 and 2024, largely due to recall-related costs and the $1.1 billion legal settlement for CPAP devices. By 2025, net income turned slightly positive, showing that Philips’ core business is recovering. Normalized EPS has been steadily positive, highlighting the underlying profitability of the business once one-time charges are excluded.

Outlook and key considerations

Philips is in a recovery phase after the CPAP recall and legal settlement. Its core health technology business remains stable, with consistent revenue and improving operating margins. Looking ahead, the company’s strategy focuses on expanding its U.S. presence, with new investments in Reedsville, Pennsylvania, and Plymouth, Minnesota, which will enhance production, research, and innovation capabilities.

Investors should note that, while the major recall settlement has been resolved, there could still be unforeseen legal or regulatory developments in the future — though none are currently reported. On the positive side, Philips’ operational efficiency is improving, normalized earnings are steadily growing, and the company has begun returning cash to shareholders through dividends, signaling confidence in cash flow stability.

Overall, Philips appears to be returning to operational health, with underlying profitability recovering and strategic investments positioning the company for long-term growth.

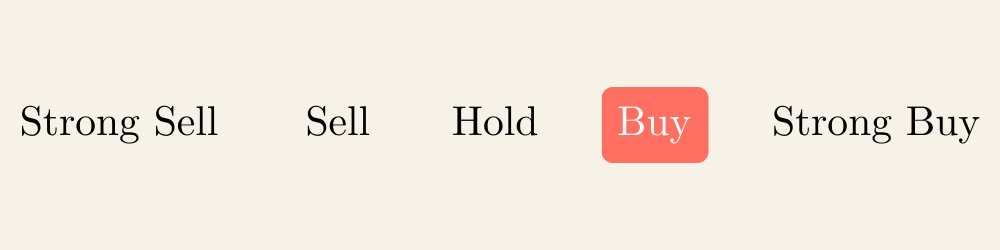

Recommendation: Buy

Philips’ stock has been weighed down in recent years due to the CPAP recall and associated legal settlements, creating a lower entry price for investors. With the major settlement now behind the company, Philips can focus fully on its core health technology business and growth initiatives, including expanding its U.S. operations and investing in innovation. Given the company’s improving operational efficiency, steady normalized earnings, and return to profitability, the stock appears attractive for investors looking for potential upside. Overall, the combination of a recovering business and a relatively undervalued stock supports a Buy recommendation.

This outlook is based on a 12- to 18-month view. This analysis is for informational purposes only and does not constitute professional investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.

Subscribe to the newsletter!

With the Augustyn Analytics Newsletter, you receive a clear monthly update featuring key business news highlights, our latest investment analyses and recommendations, a new entry from the Investor’s Guidebook explaining essential financial terms, and important updates from the Augustyn Analytics platform. Delivered just once a month, it is designed to keep investors up to date.