October 11, 2025

Overview Delta Air Lines

Delta Air Lines is one of the largest global carriers, headquartered in Atlanta, Georgia. It serves more than 275 destinations in over 50 countries. Its major hubs are Atlanta, New York, Los Angeles, and Amsterdam. Founded in 1924 as a small crop-dusting operation, Delta has grown into a leading airline. The company is known for reliability and premium customer service. It mainly competes with American Airlines and United Airlines in the U.S., and with various international carriers abroad.

In addition, Delta’s business model focuses on efficiency, a strong loyalty program (SkyMiles), and revenue from premium cabins and corporate travel. It also earns money from cargo services, aircraft maintenance, and airline partnerships through alliances like SkyTeam. After pandemic disruptions, Delta strengthened its finances. As a result, the company is improving margins, reducing debt, and investing in fleet modernization and digital infrastructure to support long-term growth.

Recent developments Delta Air Lines

On October 9, 2025, Delta Air Lines CEO Ed Bastian reported on CNBC that the airline is operating smoothly despite the federal government shutdown. However, more than 13,000 U.S. flights were delayed that week due to shortages of air traffic controllers. While Delta has not seen immediate impacts on operations, Bastian cautioned that if the shutdown continues for another 10 days, it could start to affect the airline.

On October 11, 2025, Delta announced plans to introduce new Delta One business class suites on its Airbus A350-1000 aircraft. Deliveries are expected to start in 2027. Additionally, the airline has ordered 20 planes, with options for 20 more. The suites will feature Thompson Aero VantageNOVA seats in a 50-seat layout. This upgrade will be Delta’s most premium widebody offering. It reflects the company’s strategy to increase revenue from high-end and business travelers.

On October 10, 2025, Delta and Aeromexico challenged a U.S. government decision that requires them to end their partnership by January 1, 2026. This partnership let the two airlines work together on U.S.-Mexico flights, like sharing schedules and prices, which helped both companies and passengers. Delta and Aeromexico say that ending it could cancel many flights and cost thousands of jobs. Some shared business activities would stop, but the airlines could still cooperate on marketing and frequent flyer programs. This case shows ongoing disagreements over airline rules and could affect future international partnerships.

The numbers

Three Months Ended September 30, 2025 (% = YoY):

Total revenue: $16.7B (+6%)

Passenger revenue: $13.5B (+3%)

Cargo revenue: $233M (+19%)

Other revenue: $2.9B (+24%)

Operating income: $1.68B (+21%)

Net income: $1.42B (+11%)

Basic EPS: $2.18 ($1.98 in 2024)

Diluted EPS: $2.17 ($1.97 in 2024)

Nine Months Ended September 30, 2025 (% = YoY):

Total revenue: $47.4B (+3%)

Operating income: $4.36B (+2%)

Net income: $3.79B (+45%)

Basic EPS: $5.85 ($4.08 in 2024)

Diluted EPS: $5.80 ($4.04 in 2024)

Behind the Numbers

Delta Air Lines’ financial results show strong growth both quarterly and year-to-date. For the three months ended September 30, 2025, total revenue rose 6% YoY to $16.7 billion. Passenger revenue increased 3% ($13.5B), cargo revenue jumped 19% ($233M), and other revenue, including loyalty programs, grew 24% ($2.9B).

Operating expenses rose due to higher salaries, regional carrier costs, and fees. Fuel costs fell 6%, partially offsetting the increase. As a result, operating income grew 21% YoY to $1.68 billion, and net income increased 11% YoY to $1.42 billion. Earnings per share also improved: Basic EPS $2.18 ($1.98 in 2024) and Diluted EPS $2.17 ($1.97 in 2024).

For the nine months ended September 30, 2025, total revenue reached $47.4 billion (+3% YoY). Operating income rose slightly to $4.36 billion. Net income surged 45% YoY to $3.79 billion. EPS growth was also notable: Basic EPS $5.85 ($4.08 in 2024) and Diluted EPS $5.80 ($4.04 in 2024).

Overall, both quarterly and nine-month results show that Delta is growing revenue, controlling costs, and increasing profits per share. The company benefits from diversified income streams and operational efficiency.

Source: Delta Air Lines Announces September Quarter 2025 Financial Results

Valuation

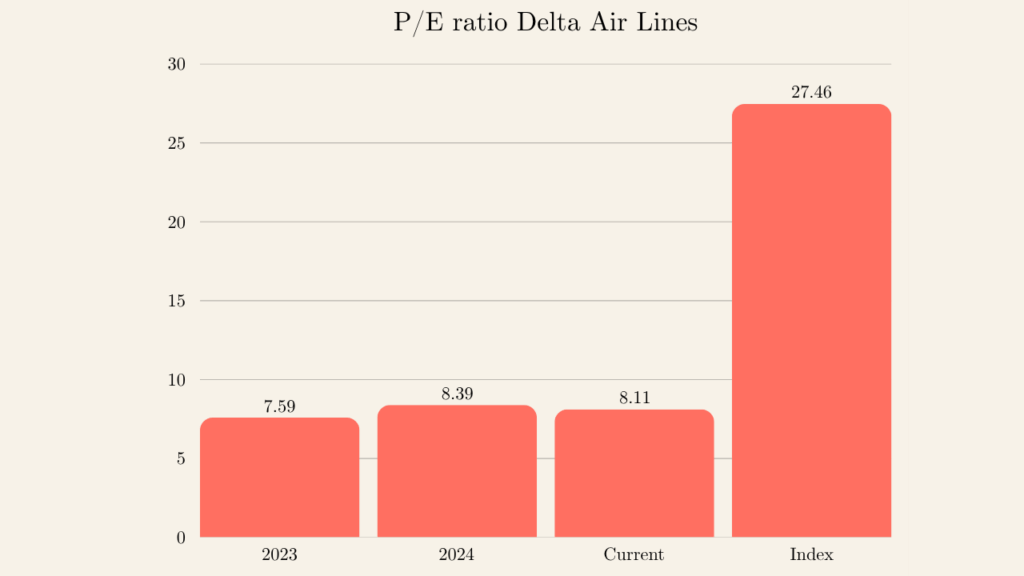

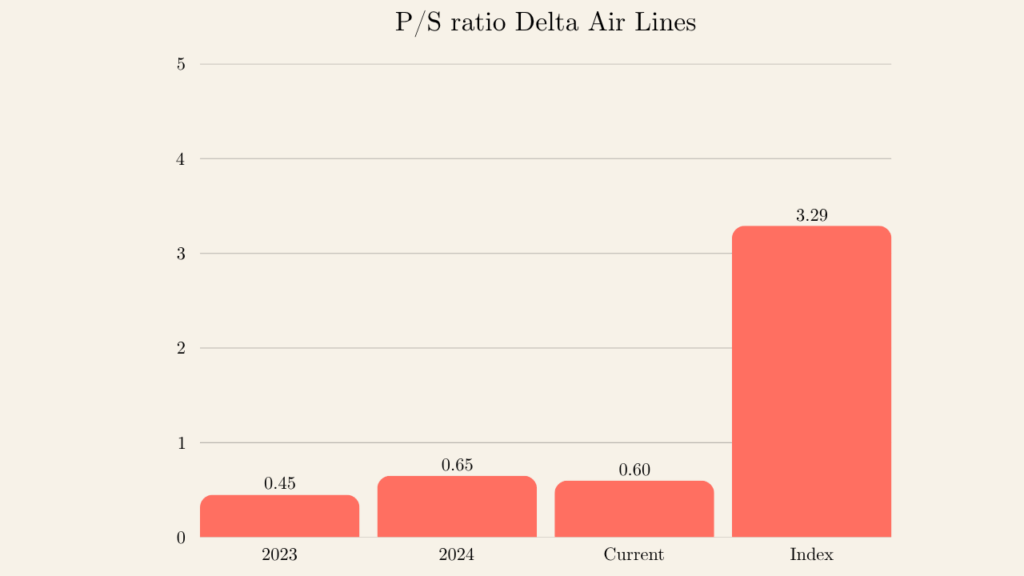

Delta Air Lines currently trades at a low valuation compared to the broader market. Its P/E ratio over the past few years (2022–2024) has been around 7–8, far below the S&P 500 index P/E of 27.46, showing it is cheaper relative to market earnings. On a revenue basis, Delta’s Price/Sales ratio is around 0.6, well below the S&P 500 P/S of 3.29, indicating the stock is also undervalued relative to revenue. Overall, the combination of low P/E, strong revenue growth, and improving profitability makes Delta attractive for investors seeking value in the airline sector.

Source: Morningstar October 10, 2025

Outlook & key considerations

Delta’s short- and long-term outlook remains positive, but with some risks. Passenger demand is expected to remain strong as air travel continues to recover globally. The airline’s focus on premium cabins, loyalty programs, and operational efficiency should support revenue growth and profitability. Investments in fleet modernization, including the new A350-1000 suites, are likely to enhance the customer experience and attract higher-yield travelers.

Despite these positive trends, several factors could impact results. Fuel prices, economic slowdowns, and labor costs are key risks, as they can affect margins quickly—airlines are highly labor-intensive, and rising wages or strikes can significantly impact profitability. Additionally, airline operations are sensitive to government regulations and potential disruptions, such as strikes or travel restrictions.

Delta’s P/E ratio is around 7–8, which is low compared to the S&P 500 index P/E of 27.46. On average, U.S. airline peers have a P/E in the 8–12 range, showing that Delta trades at the lower end of its sector. This combination of low valuation and strong financial results suggests that Delta may be undervalued and attractive for investors.

Recommendation: Buy

We recommend Buy – Delta Air Lines offers a compelling combination of strong financial performance, growing revenue, and operational efficiency, while trading at a low valuation relative to both the broader market and airline peers. Recent developments, such as fleet modernization and premium cabin expansion, support long-term growth. Although risks like fuel costs, labor expenses, and industry sensitivity remain, the company’s diversified income streams and improving profitability make it an attractive investment for value-oriented and growth-focused investors.

This outlook is based on a 12- to 18-month view. This analysis is for informational purposes only and does not constitute professional investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.

Keep learning with us!

Stay informed and grow as an investor! Follow Augustyn Analytics on Instagram and TikTok for daily business news, short educational videos, and practical tips to help you make smarter investment decisions.