August 3, 2025

ASML overview

ASML is one of the most important and influential technology companies in the world, despite its relatively low public profile.

Headquartered in the Netherlands, ASML designs and manufactures machines that are essential for producing advanced computer chips. Its technology enables the creation of the tiny, powerful semiconductors found in nearly every modern electronic device.

These chips power a wide range of technologies — from smartphones, laptops, and gaming consoles to electric vehicles, medical equipment, industrial machinery, and artificial intelligence systems.

ASML is currently the only company capable of building extreme ultraviolet (EUV) lithography machines — a key tool for producing the most advanced chips. This unique position makes ASML a critical supplier to major semiconductor manufacturers such as TSMC, Samsung, and Intel.

Recent developments

High‑NA EUV machines move toward production

ASML is preparing to ship its next-generation High‑NA EUV systems, with Intel set to begin early production in 2026. These tools promise even greater precision, helping chipmakers shrink transistors further while improving efficiency.

Strong demand and a growing order book

Despite export restrictions, ASML continues to see robust demand. In its Q2 2025 earnings report, the company posted new orders worth €9.2 billion, far exceeding expectations. Roughly €1.9 billion of that came from China, where demand for ASML’s deep ultraviolet (DUV) machines remains strong.

However, EUV machine exports to China are restricted under U.S.-led regulations aimed at limiting China’s access to advanced chipmaking capabilities. These rules, which came into effect in 2023 and were further tightened in 2024, prevent ASML from shipping its most advanced lithography systems — particularly EUV and certain DUV models — to Chinese customers.

Geopolitical risks add uncertainty

ASML recently warned that it can no longer guarantee growth in the short term amid rising trade tensions. A new U.S. proposal includes tariffs on European semiconductor exports, directly impacting ASML and its customers. This adds further uncertainty to the near-term outlook, as geopolitical developments continue to shape the global tech landscape.

Chinese competition remains limited

China has announced efforts to develop its own EUV machines, with trial production expected as early as 2026. However, ASML’s leadership and industry analysts remain skeptical, citing major technical challenges in optics, mirrors, and resists that may delay true competitiveness by many years.

The numbers

Market Capitalization: $271.24 billion

Shares Outstanding: 393.20 million

Price-to-Earnings Ratio (Normalized): 26.36

Price-to-Sales Ratio: 7.74

Dividend Yield (Trailing): 1.04%

Dividend Yield (Forward): 1.07%

52-Week Price Range: $578.51 – $945.05

Normalized EPS (2025): $24.09

Diluted EPS (2025): $25.01

Source: Morningstar august 1, 2025

Behind the numbers

ASML has a market capitalization of $271.24 billion, based on 393.20 million shares outstanding. This substantial market value reflects strong investor confidence and underscores the company’s significant position in the global technology sector.

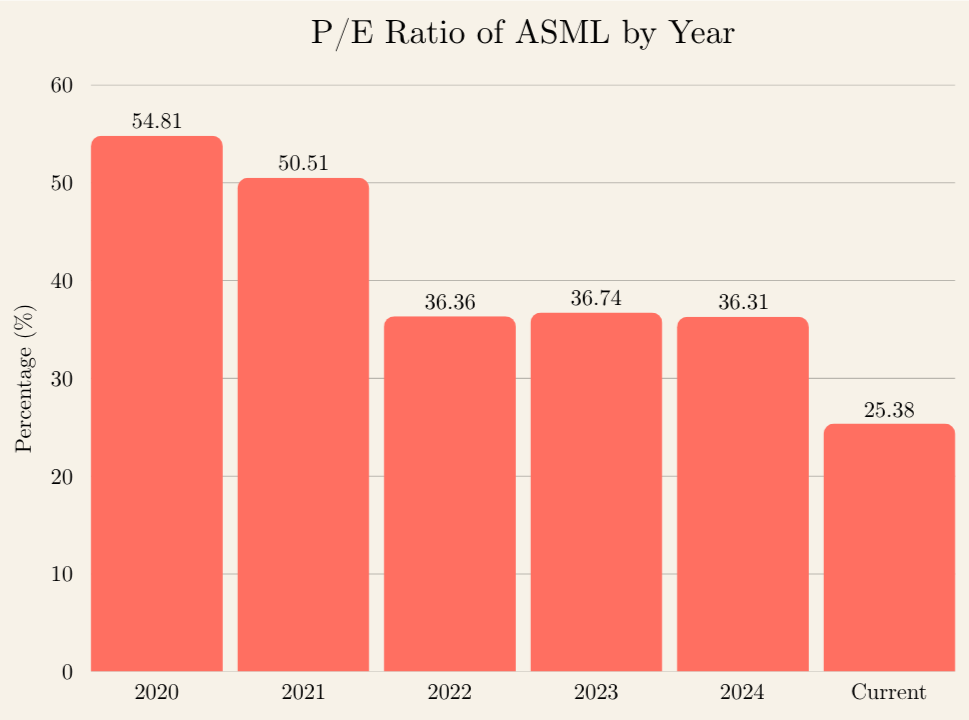

Its financial indicators reflect both strength and sensitivity to broader global forces. ASML’s 2025 earnings remain solid, with a diluted EPS of $25.01 and a normalized EPS of $24.09. Since peaking in 2020, ASML’s price-to-earnings (P/E) ratio has steadily declined. This suggests that investors are now paying less for each dollar of ASML’s earnings compared to a few years ago — a result of stronger earnings growth, more cautious market sentiment, or a combination of both. Despite the lower valuation, ASML remains a key player in the global semiconductor industry.

While ASML’s dividend yield of just over 1 percent is modest compared to more mature sectors, it is typical for a high-growth technology company. Notably, ASML’s dividend yield has steadily increased over the past three years, reflecting confidence in its long-term earnings power and financial stability.

One standout figure is the 52-week trading range — from $578.51 to $945.05 — representing a swing of over 60%. For a company with a market cap of this size, such volatility is unusually wide. It highlights the market’s shifting expectations around ASML, influenced by macroeconomic factors, export controls on advanced chip equipment, and ongoing geopolitical uncertainty. This volatility serves as a reminder of the high-stakes environment in which ASML operates.

Outlook and key considerations

ASML’s outlook remains positive due to its near-monopoly in the specialized EUV lithography market, making it essential to major chipmakers like TSMC, Samsung, and Intel. The company’s strong intellectual property, high barriers to entry, and ongoing R&D investments support its leadership and financial strength.

Recently, ASML cautioned that short-term growth is uncertain amid rising trade tensions and proposed U.S. tariffs on European tech exports. With semiconductor equipment now included in the latest tariff measures, geopolitical risks have become a more immediate concern for ASML and the broader industry.

Despite these factors, ASML’s lower price-to-earnings ratio compared to past years makes the stock more attractive, reflecting market caution but also a better entry point. Backed by steadily growing earnings, ASML’s strong position and fundamentals indicate solid long-term growth potential — even if short-term growth may slow due to new tariff pressures, this does not diminish the company’s broader trajectory if it continues to innovate and manage risks effectively.

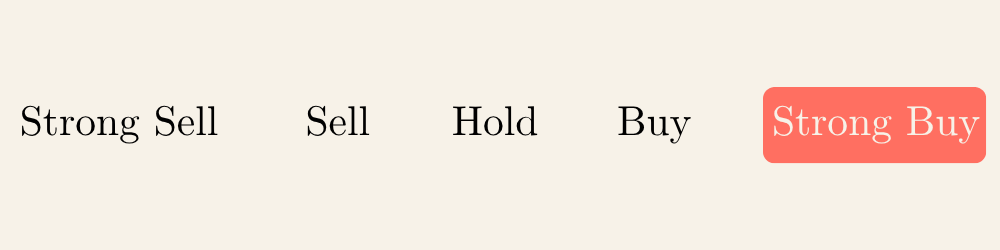

Recommendations: Strong buy

ASML is a strong buy, supported by its dominant role in advanced chip manufacturing, consistent earnings growth, and continued technological leadership. The stock’s current lower valuation presents an appealing entry point, offering meaningful upside as the company maintains strong financial performance.

Although geopolitical risks add near-term uncertainty, ASML’s unique market position and focus on innovation make it well-positioned for long-term growth. Long-term investors should consider adding ASML to their portfolio.

This outlook is based on a 12- to 18-month view. This analysis is for informational purposes only and does not constitute professional investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.